Explore 5 smart strategies UK homeowners can use to stay in control of your mortgage costs.

Small financial planning techniques made at the right time can knock thousands of £££ off the total cost of your mortgage and free up equity for future goals.

Tip 1: Keep monthly costs comfortable – even when life changes

Why it matters: Life rarely follows a straight line, and events such as redundancy, having a child, long-term illness or relationship breakdown can suddenly squeeze household cashflow.

A minimum repayment that felt manageable at completion of your new purchase or remortgage can become uncomfortable overnight if your income dips or essential outgoings rise.

Acting early – by reviewing your budget, trimming optional spending, and contacting your broker or lender before a payment is missed – gives you far more options to work with.

The sooner you foresee something that could impact your mortgage, then you have more flexibility & this could result in less stress for your household.

Plan for life’s

‘little surprises’

- Stress-test your budget before you commit:

- Aim for a repayment that would still be affordable if your income dropped by 20%.

- Stress-test your mortgage rate before you commit:

- Ensure you could still repay your mortgage monthly minimum payment if your mortgage rate increased by at least 3%.

- Build an ‘overpayment reserve’:

- Check with your lender whether making overpayments to your mortgage in earlier months allows you to reduce or pause mortgage payments for a short period in future, after you have built an overpayment reserve.

- Build a ‘mortgage emergency fund’:

- If your lender does not allow for an overpayment reserve, perhaps consider a dedicated savings pot with a target of 3-6 months of mortgage repayments.

- Keeping this money aside could be easy-access funds if there was a sudden change to your situation.

- Monitoring LTV when starting a product transfer:

- As your current mortgage rate ends, check the lender’s valuation of your home is accurate or if you are close to a LTV (loan-to-value) boundary.

- If you think the lender has undervalued your home, you may be able to request a revaluation before the new product start date to access better products.

- If you are close to the LTV boundary (e.g. 77%) then make an overpayment to reduce your mortgage to below the next LTV boundary (e.g. 77% to <75%) to potentially unlock a cheaper mortgage rate.

- Requesting a term extension:

- If your current mortgage term is lower than the maximum available for customers of your age, you may request to extend your mortgage term to reduce the monthly minimum repayments.

- However, this would increase the total interest repaid over the course of your mortgage term and could extend the end date of repayments into your planned retirement.

- It is advised that you seek professional advice from a mortgage advisor before considering extending the term of an existing mortgage.

If you’d like specialist, FCA-regulated guidance on any of the strategies above, simply send us a quick mortgage enquiry. Our qualified mortgage advisor will review your circumstances, outline your options and help you decide the most cost-effective way forward.

Get help from SWMTip 2: Strategic overpayments – shrink your debt faster

Why it matters: Overpayments are voluntary extra payments paid on top of your contractual monthly repayment. As the money goes straight towards reducing the capital balance, every pound overpaid stops the future interest that would have been charged on that pound.

Most mainstream UK lenders let you pay in up to 10 % of your outstanding balance each policy year without triggering Early Repayment Charges (ERCs). It is always best to discuss planned overpayments with a mortgage advisor if you intend to make any large individual payments.

Below are two practical ways to deploy this power, answers some questions below to see what option is best for you.

Is overpaying right for you? Use our quick-decision questionnaire:

Q1: Do you regularly clear higher-rate debts?

(e.g. credit cards, overdrafts, personal loads, hire purchase)

Q2: Is your emergency fund at least three months’ living costs, including your mortgage payment?

Q3: Is your mortgage rate higher than the after-tax return you expect from investing?

(e.g. Stocks & Shares ISA or personal pension)

Q4: Do you prefer guaranteed savings over potential market gains?

Q5: Can you commit to a regular overpayment every month?

Recommendation: Prioritise those first. Your mortgage cost could be lower than these other commitments. You could benefit from using excess funds to clear these other debts first. If you want specific advice, please book a call with us.

Recommendation: Build this buffer before overpaying on a mortgage. Life can change suddenly & unexpectedly. Having 3-6 months of easy-access savings to cover an unforeseen life event could be better than overpaying towards your mortgage. Book a call with us to discuss a plan built around your specific needs & lifestyle.

Recommendation: Overpaying is likely the smarter move. If you’d like us to review your circumstances, then please book a call.

Recommendation: Occasional, ad hoc overpayments might strike a balance between investing and managing your debts. However, long-term investing in alternative financial instruments (such as bonds, property or equities) could provide a greater return when compared with overpayments on your mortgage £ per £. Book a call with us if you want to discuss your investment options.

Recommendation: Choose to overpay directly as-and-when you can – typically you can do this via online/mobile banking or calling your lender for a single card payment over the phone. Always check if your overpayment will incur ERCs before you finalise any payment. Book a call with us if you are uncertain about making an overpayment.

Recommendation: Choose to overpay by updating your direct debit to an amount higher than your monthly minimum. This will automatically overpay your mortgage each month. Always check if your overpayment plan will incur ERCs before you finalise the adjustment to your direct debit. Book a call with us if you are uncertain about making an overpayment.

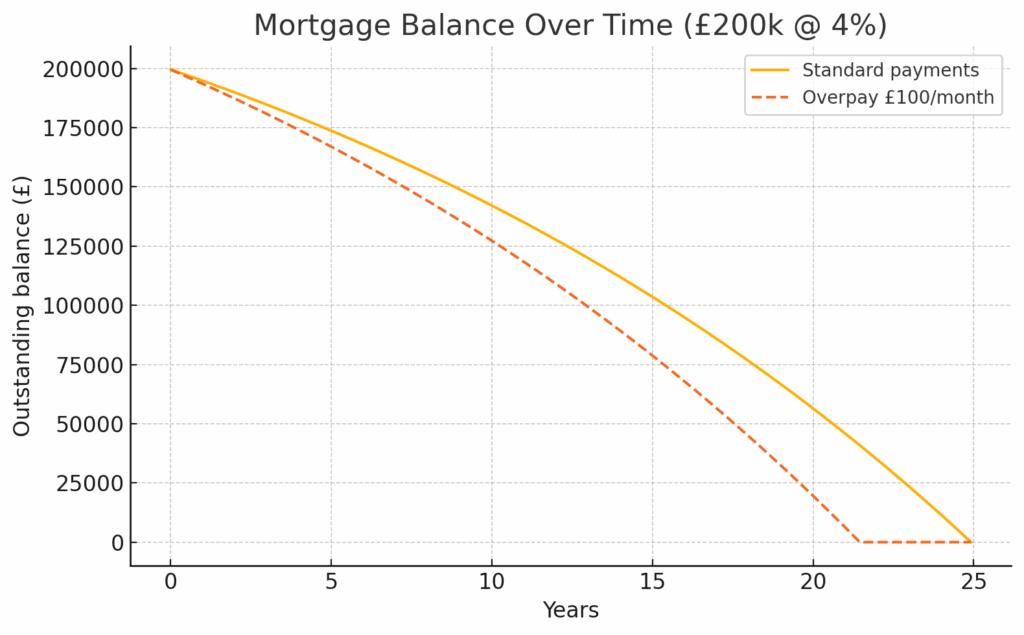

Option A: Regular overpayments – the ‘set-and-forget’ habit

- How to do it: Log in to your online banking portal or contact customer services to increase your direct debit payment for your mortgage (e.g. from £950 to £1,050 per month).

- Impact: Even a modest £100 extra each month on a £200,000, 4 %, 25-year mortgage trims around £17,400 in interest and wipes 3+ years off the term (see below).

- Flexibility: Need the cash back? It may be possible to release this increased equity in your property with additional borrowing through a further advance or capital-raising remortgage. SWM can guide you on whether this is possible for your circumstances.

- Motivation hack: Adjusting the direct debits reduces the time & effort compared to regularly making manual overpayments. You can also set a calendar alert every six months to see how far the projected “mortgage-free date” has moved forward. Watching the gap close is highly addictive!

Option B: Sporadic overpayments – the one-off hammer blow

- Sources: Annual bonus, inheritance, matured ISA, vested shares, crypto gains, even a lottery win … When you receive a significant windfall income, consider reducing your mortgage debt.

- Check before you send: Contact your mortgage lender to confirm how much of your annual overpayment allowance remains for the current policy year.

- Timing matters: Many providers reset the allowance on the anniversary of completion, not 1 January. Paying a lump sum one week too early can attract an avoidable ERC.

- Keep proof: File the lender’s confirmation email/PDF in your mortgage folder; it’s your receipt if questions arise later.

- Other use of funds: If your windfall income exceeds 10% of your mortgage balance, consider alternative financial strategies – such as contributing to a Stocks & Shares ISA or personal pension to utilise other unused annual allowances.

Try our calculator to model how different overpayment amounts change your term and total interest.

Tip 3: Watch your equity snowball & make it benefit you

Why it matters: Equity is the portion of your home you truly own = current property value, minus your outstanding mortgage balance.

If you have a capital & interest repayment mortgage, every monthly payment chips away at the debt. If we assume that over the long-run property prices often rise, then this combines to lower your loan-to-value (LTV).

Lower LTV on your home unlocks 3 big wins:

Equity win 1: Manage your mortgage well and you could have positive equity

Significant positive equity lets you raise cash while keeping mortgage-rate pricing – via a further advance, a capital-raising remortgage or even a second-charge loan. The money can fund an extension, school fees, a buy-to-let deposit or any other lender-approved purpose.

To understand if you have positive equity, check this:

- Positive equity – your home is worth more than you owe, shielding you if prices dip.

- Negative equity – balance exceeds value; very few lenders refinance above 100 % LTV, so you could be stuck on a punishing SVR until the market recovers. You may be a ‘mortgage prisoner’ and should contact a mortgage advisor as soon as possible.

Stay on the right side:

- Make overpayments where possible.

- Keep a maintenance fund, so the property’s condition (and therefore valuation) doesn’t decline.

- Keep invoices & receipts when you make home improvements, as surveyors could use this to improve the valuation of your home.

- Aim to leave yourself at least one LTV band of headroom after any cash-out.

Done well, you get the funds you need today and preserve your ability to secure cheaper deals tomorrow.

Equity win 2: Lenders typically focus on LTVs for setting mortgage rates, more than mortgage balances

| Loan-to-value (LTV) | Products | What happens for you? |

| >90% | Limited lenders, higher stress-tests, most expensive | Focus on overpaying your mortgage to below 90% LTV |

| 75-90% | Mainstream deals appear, slightly more expensive | Mortgage rates typically improve every 5% you drop on LTV |

| 60-75% | “Core” range for most banks | You’re close to the best products available |

| <60% | Premium, low-risk tier with the cheapest products | At very low LTV, you will likely get the choice of the best rates from every lender |

Tip: A free AVM (automated valuation model) from your own lender or Zoopla can be enough evidence to trigger a better product transfer.

If their desktop value is inconclusive and you’re close to a LTV boundary, ask for a paid-for survey (often £100–£250) and benefit from the potential lower repayments.

Equity win 3: Release stored equity for life’s big moments

Releasing some of the equity you’ve built up over time can be cheaper and more tax-efficient than taking unsecured credit.

| Option | What is this? | When it works best for you |

| Further advance | Additional loan as a ‘top-up’ from your current lender that opens a new sub-account at current rates. | If you need quick cash for a refurb project, car, school fees, debt consolidation. You will be limited by your lender’s criteria & LTV of the new overall borrowing. |

| Capital-raising remortgage | Move the whole mortgage to a new lender and borrow extra with all borrowing at the same current rates. | Best applied for at the end of your current mortgage product to avoid ERCs. Although this involves a full legal process, this can be easier than managing new sub-account(s). |

| Second-charge loan | Best envisaged as a small loan using your home as collateral as extra safety for the lender. | Ideal when your current lender will not allow for additional borrowing and midway through a product period, so would incur significant ERCs. |

Make your property’s equity benefit you

Typical uses of additional borrowing:

- Extension or loft conversion (adds value & comfort)

- University fees or private schooling

- Deposit for a buy-to-let or holiday let

- Early inheritance gift to children

Tax-free boost when you downsize:

Selling your main home qualifies for Principal Private Residence (PPR) relief. Under current UK rules, any capital gain is exempt from CGT.

Example: Sell at £450,000 with £90,000 left on the mortgage → net proceeds ≈ £360,000 cash released before legal fees & moving costs, entirely tax-free.

Use your equity released to buy a smaller property outright to have a mortgage-free home in retirement, top up pensions or bolster your savings.

Considering a further advance or planning to downsize?

Our advisers can model your mortgage costs, check lender criteria, and discuss what your options are:

Explore the typical mortgage journey for our clientsTip 3: Watch your equity snowball & make it benefit you

Why it matters: Need extra cash but happy where you live? If you still meet residential affordability, you can borrow against your growing equity at mortgage-level pricing instead of resorting to costly personal loans or credit cards.

This is not the same as equity release – as these products are designed for older borrowers who wish to extend their borrowing longer into retirement. We offer specialist equity release advice, so please do get in touch if you or someone you know needs equity release advice ahead of retirement.

I need equity release advice 📧